Therapy Isn’t Just the Copay - Here’s What Else You’re Really Paying

You walk into your therapist’s office, swipe your insurance card, and pay your $30 copay. Feels simple, right? But that $30 is just the tip of the iceberg. If you think that’s all you’ll pay for therapy this year, you’re setting yourself up for a nasty surprise. The real cost of therapy includes your deductible, coinsurance, out-of-pocket maximum, session frequency, and whether your provider is in-network or out-of-network. And none of that shows up on your insurance card.

According to Thriveworks’ 2024 analysis of over 175,000 therapy sessions, the average cost per session without insurance is $143.26. With insurance, your out-of-pocket cost can range from $0 to $100+ per session - and that’s before you even factor in how many sessions you’ll need. Most people see improvement after 12 to 16 sessions. That means even at $30 per session, you’re looking at $360 to $480 just for the basics. But what if your deductible hasn’t been met? What if you’re on a coinsurance plan? What if you live in North Dakota, where therapy costs $227 per session?

Know Your Plan Type - Copay, Deductible, or Coinsurance?

Your insurance plan doesn’t work the same way as your friend’s. There are three main structures, and each changes how you pay.

- Copay plans: You pay a fixed amount per session - say $30. Easy, right? But only if your deductible is already met. If it’s not, you pay the full session rate until you hit that number.

- Deductible plans: You pay 100% of the session cost until you’ve spent a set amount - like $1,500 - in a year. If your therapist charges $125 per session, you’ll pay that full amount for 12 sessions before insurance kicks in. That’s $1,500 out of pocket before you even see a $30 copay.

- Coinsurance plans: After your deductible, you pay a percentage - usually 20% to 40% - of what the insurance allows. If your plan allows $125 per session and you pay 20%, that’s $25 per session. But if your therapist charges $200 and your insurance only covers $125, you pay the difference too.

Most people assume their copay is their total cost. It’s not. A $30 copay on a coinsurance plan might mean you’re paying $25 per session after your deductible - but only if you’ve already spent $3,000 that year. That’s a big difference.

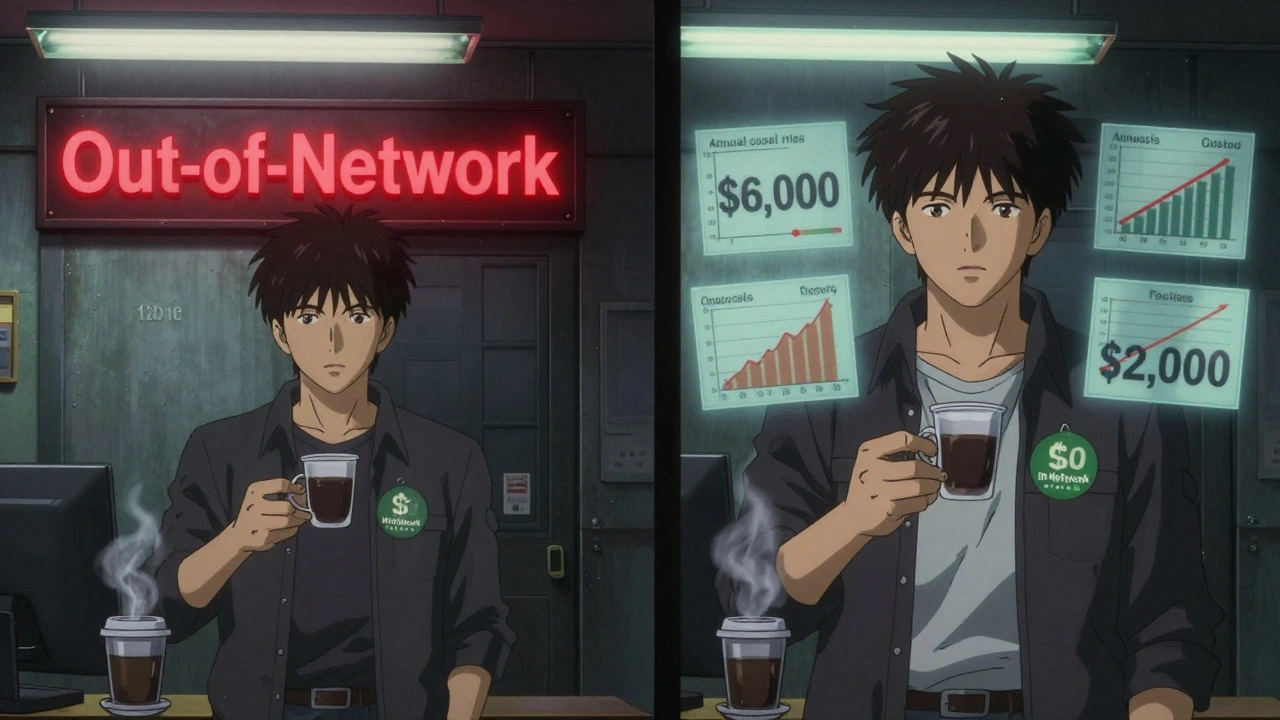

Out-of-Network Therapy Can Double Your Costs

If your therapist doesn’t take your insurance, you’re on your own. You pay the full fee upfront, then submit a claim for partial reimbursement. But here’s the catch: your insurance doesn’t pay based on what the therapist charges. They pay based on their allowed amount - which is often much lower.

For example: your therapist charges $180 per session. Your insurance’s allowed amount for that service is $120. You pay $180, then get reimbursed 50% of $120 - so $60 back. That means you’re still paying $120 out of pocket per session. That’s 80% more than if you’d chosen an in-network provider.

Alma’s 2023 data shows out-of-network patients pay 40-50% of the session cost after deductible, while in-network patients pay 20-30%. That gap adds up fast. If you’re doing 20 sessions at $150 each, out-of-network could cost you $6,000 before hitting your out-of-pocket max. In-network? Maybe $2,000.

Location Matters More Than You Think

Therapy isn’t priced the same everywhere. Thriveworks found that in New York, the average session is $176. In North Dakota, it’s $227. That’s a 29% difference. If you’re on a 20% coinsurance plan, that’s $35.20 per session in New York - but $45.40 in North Dakota. Multiply that by 20 sessions, and you’re paying $184 more just because of where you live.

And it’s not just big cities. Rural areas often have fewer providers, which drives prices up. If you’re in a small town with only one therapist who doesn’t take insurance, you’re stuck paying full price - and that’s not always negotiable.

Your Out-of-Pocket Maximum Isn’t a Free Pass

Insurance companies set an annual out-of-pocket maximum - the most you’ll pay for covered services in a year. In 2024, that cap is $9,350 for individuals and $18,700 for families. Sounds like a safety net, right?

But here’s what most people don’t realize: not all services count toward the same deductible. Some plans have separate deductibles for medical and mental health care. So even if you’ve hit your $9,350 cap for doctor visits and prescriptions, you might still owe $1,500 more just for therapy.

And if you’re on a high-deductible plan with a $6,000 deductible and 30% coinsurance, you could hit your out-of-pocket max after 25-30 sessions - but only if your therapist charges $150 or more per session. If you’re seeing someone for $100, you might need 40 sessions to hit that cap. That’s over a year of therapy.

Medicare and Medicaid Are Different - Here’s How

If you’re on Medicare, you pay 20% of the approved amount after meeting your Part B deductible. Thriveworks reports the average Medicare patient pays $28.65 per session. That’s low - but only if your therapist accepts Medicare assignment. Many don’t. If they don’t, you pay the full fee and get nothing back.

Medicaid usually has little to no copay for therapy. But not all therapists accept it. In some states, fewer than 30% of private therapists take Medicaid. So even if your copay is $0, you might not find a provider.

Medigap Plan G helps cover Medicare’s 20% coinsurance - but it costs $120-$200 a month in premiums. So you’re trading a $28 copay for a $150 monthly bill. It’s a trade-off.

Sliding Scale and Low-Cost Options Exist - If You Know Where to Look

Not everyone has insurance. And even if you do, your deductible might be too high to make therapy affordable. That’s where alternatives come in.

- Sliding scale fees: About 42% of private therapists offer income-based pricing. You might pay $40 instead of $120 if your income qualifies. You’ll need to provide proof - tax returns, pay stubs - but it’s worth asking.

- Open Path Collective: A nonprofit network that connects uninsured people with therapists who charge $40-$70 per session. One-time membership fee of $60.

- University training clinics: Graduate students in psychology programs offer therapy under supervision at 50-70% off market rates. Sessions might be 50-90 minutes long. You’re not getting a licensed therapist, but you’re getting quality care at a fraction of the cost.

These aren’t magic fixes - waitlists are long, and availability is limited. But they’re real options that can cut your annual cost from $2,000 to $500.

Build a Real Budget - Not a Guess

Here’s how to calculate your total therapy cost step by step:

- Find your plan type: Is it copay, deductible, or coinsurance? Call your insurer or check your member portal.

- Check your deductible: How much have you paid so far this year? How much is left?

- Know your session cost: What does your therapist charge? What’s the insurance allowed amount?

- Estimate sessions: Most people need 12-16 sessions for improvement. Complex issues like PTSD or chronic anxiety may need 20-30.

- Calculate Phase 1 (pre-deductible): Full session cost × sessions until deductible is met.

- Calculate Phase 2 (post-deductible): Copay or coinsurance × remaining sessions.

- Add your premium: Multiply your monthly insurance payment by 12.

- Check your out-of-pocket max: Will you hit it? If so, your costs stop there.

Example: You have a $1,500 deductible, $40 copay after deductible, and your therapist charges $125/session. You plan for 20 sessions.

- Phase 1: $125 × 12 sessions = $1,500 (meets deductible)

- Phase 2: $40 × 8 sessions = $320

- Total: $1,820

Without insurance? $2,500. With insurance? $1,820. That’s a $680 savings - but only if you know how to calculate it.

When to Start Therapy - Timing Can Save Money

Insurance plans reset on January 1. If you’re close to hitting your deductible, waiting until January might save you hundreds. But if you’re struggling, don’t delay care for money reasons. Instead, use the reset to your advantage.

For example: if you’ve spent $1,200 on physical therapy and your mental health deductible is $1,500, you only need $300 more in medical expenses to hit it. A $100 MRI or a $200 prescription can push you over. Then your therapy sessions drop to $40 each.

Any covered medical service counts toward your deductible - not just therapy. So if you’re already seeing a doctor for back pain or diabetes, you’re already building toward your mental health deductible. You just need to track it.

Final Tip: Ask for a Cost Estimate Before You Start

Therapists are not required to give you a cost estimate - but many will if you ask. Call the billing department. Say: “I’m planning 20 sessions. Can you tell me what my out-of-pocket cost will be based on my insurance?”

Use tools like Alma’s free cost estimator or Rula’s calculator. They pull your plan data and show you what you’ll pay month by month. Nearly 40% of patients say they didn’t know their copay until after their first session. Don’t be one of them.

Therapy is worth it. But you shouldn’t have to go broke to get it. Know your numbers. Plan ahead. And don’t let the copay fool you - it’s never the whole story.

Is my copay the only thing I pay for therapy?

No. Your copay is just one part of the cost. You may also pay your deductible, coinsurance, and out-of-pocket maximum. If you haven’t met your deductible yet, you pay the full session fee. If you’re on a coinsurance plan, you pay a percentage of the allowed amount after your deductible. And if your provider is out-of-network, you might pay more than the copay even after meeting your deductible.

How do I know if my therapist is in-network?

Call your insurance company and ask for a list of in-network mental health providers. You can also check your insurer’s website or app - most have a provider directory. If your therapist says they’re in-network, ask them to verify it with your plan. Sometimes providers get dropped from networks without telling patients.

What if I can’t afford therapy even with insurance?

Many therapists offer sliding scale fees based on income - ask them directly. You can also use Open Path Collective for $40-$70 sessions, or check with local universities for low-cost training clinics. Community mental health centers often offer free or low-cost services too. Don’t assume therapy is out of reach - there are options if you look.

Does Medicare cover therapy?

Yes. Medicare Part B covers 80% of the approved amount for therapy after you meet your Part B deductible. You pay the remaining 20%. If your therapist accepts Medicare assignment, you’ll pay about $28.65 per session on average. If they don’t, you may pay the full fee and get nothing back. Medigap Plan G can cover that 20% coinsurance, but it adds a monthly premium.

Can I use my HSA or FSA for therapy?

Yes. Therapy is a qualified medical expense under both Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). You can use pre-tax dollars from these accounts to pay for copays, coinsurance, or full session fees - even if you haven’t met your deductible yet. This can save you 20-30% on your out-of-pocket costs depending on your tax bracket.

Why does my out-of-pocket cost keep changing?

Your cost changes based on how much you’ve paid toward your deductible and coinsurance. Early in the year, you pay full price. Once you hit your deductible, you pay a copay or coinsurance. If you hit your out-of-pocket maximum, you pay nothing more for covered services. Also, if your therapist changes their fee or your insurance updates their allowed amount, your cost can shift. Always check your explanation of benefits (EOB) after each session.

Shannara Jenkins

Wow, this is such a needed post. I thought my $25 copay was it - turns out I paid $1,200 just to hit my deductible before the copay even kicked in. I didn’t even know my plan had a separate mental health deductible. Thanks for laying this out so clearly.

Elizabeth Grace

I cried reading this. I’ve been skipping sessions because I thought I was ‘fine’ - but really I was just broke. Now I’m calling my therapist to ask about sliding scale. I’m not proud, but I’m done pretending.

Alicia Marks

This is gold. Save this post.

Laura Baur

The structural inequities embedded in mental healthcare financing are a direct reflection of late-stage capitalist pathology. You cannot commodify human suffering without creating perverse incentive structures that prioritize profit over healing. The fact that a person in North Dakota pays 29% more for therapy than someone in New York isn’t an anomaly - it’s a feature of a system that treats mental health as a luxury, not a right. And don’t get me started on how Medicaid’s low reimbursement rates create provider deserts in low-income communities - this is systemic neglect dressed up as policy.

Sliding scale options are Band-Aids on bullet wounds. What we need is universal mental healthcare coverage, fully integrated into Medicare for All, with mandatory provider participation and transparent pricing algorithms. Until then, we’re just rearranging deck chairs on the Titanic while people drown in silence.

Jack Dao

Wow, so you’re telling me I’m supposed to *do math* to afford therapy? What a concept. I guess I should’ve majored in finance instead of psychology. My therapist charges $200, I have a $6,000 deductible, and I make $42k a year. Guess I’ll just keep being depressed. At least it’s free.

Also, why are you so obsessed with insurance? Just pay cash. If you can’t afford it, you’re not ready for therapy. Simple.

Paul Keller

While I appreciate the data-driven breakdown, I must point out that the entire premise is flawed. Therapy, as a market-based service, is subject to the same supply-and-demand dynamics as any other profession. The fact that you’re surprised by the cost reflects a deeper cultural delusion - that emotional labor should be cheap, or even free. The therapist is not a charity worker; they’ve spent a decade in graduate school, carry malpractice insurance, and pay rent in cities where a studio apartment costs more than your monthly car payment. The real issue isn’t insurance complexity - it’s the societal expectation that mental health support should be subsidized by the provider’s personal sacrifice. If you want affordable therapy, advocate for public funding, not guilt-trip clinicians into offering discounts. And yes, I’ve been in practice for 18 years - I’ve seen this cycle repeat endlessly.

Rebecca M.

OMG I JUST REALIZED I’VE BEEN PAYING $180 A SESSION FOR 6 MONTHS AND I’M ONLY 1/3 OF THE WAY TO MY DEDUCTIBLE 😭😭😭 I’M SO DONE WITH THIS SYSTEM

Lynn Steiner

USA is the only country where you need a degree in finance just to get help for your trauma. In India, my cousin got therapy for $5 a session through the government. Here? I need a spreadsheet and a second job. This isn’t healthcare - it’s extortion with a waiting room.

dave nevogt

I’ve spent the last three years in therapy, and this post hit me like a slow wave. What no one tells you is that the cost isn’t just financial - it’s emotional labor to navigate the system. You have to become your own advocate, your own billing clerk, your own insurance detective. You’re not just healing your mind - you’re fighting a bureaucracy that doesn’t want you to succeed. And yet, we still show up. Every week. Even when we’re exhausted. Even when we’re broke. That’s the quiet resilience no one writes about. I’m not grateful for the system - I’m grateful for the therapists who still show up for us anyway.

Arun kumar

this is so true in india too we have no insurance for mental health and therapy cost is high but many student clinics are helping. i wish more people know about it

Zed theMartian

Let me guess - you’re one of those people who thinks therapy is ‘self-care’ and not ‘weakness.’ Congratulations, you’ve bought into the wellness-industrial complex. Real men don’t talk to strangers about their feelings. They go to the gym, drink protein shakes, and bottle it up until they explode. This article is just corporate America selling you a $120/hour placebo while your real problems - unemployment, loneliness, climate grief - go unaddressed. Therapy won’t fix capitalism. But it’ll make you feel better about being broke.

Ella van Rij

So… I paid $900 in 2023 for therapy and just found out my ‘$30 copay’ was actually coinsurance after a $3k deductible? And I thought I was doing so well?? 😂😂😂 I need to send this to my mom. She’s gonna have a heart attack.

ATUL BHARDWAJ

in nigeria we pay cash no insurance no problem. therapist is friend who studied psychology. cost is 2000 naira 1.50 usd. therapy is human not business

Steve World Shopping

Based on the WHO’s 2023 Mental Health Gap Action Programme (mhGAP) framework, the structural underfunding of outpatient mental health services in the U.S. reflects a chronic misallocation of public health resources, wherein behavioral health is siloed from primary care, resulting in fragmented care delivery and inflated transactional costs. The absence of integrated care pathways exacerbates provider burnout and patient attrition - a phenomenon empirically correlated with socioeconomic stratification. Until policy interventions align reimbursement models with population health outcomes rather than fee-for-service incentives, the current paradigm will remain unsustainable.

Paul Keller

Actually, Laura - your point about systemic neglect is valid, but you’re missing the human layer. People don’t need more policy papers. They need someone to say, ‘I see you’re struggling, and here’s how you can get help today.’ That’s what this post does. It’s not perfect, but it’s actionable. And sometimes, actionable beats philosophical.