Why Prescription Costs Keep Rising and Where Apps Step In

Sticker shock isn't rare at the pharmacy counter. Prices for basic prescriptions have been inching up for years, and for anyone dealing with chronic conditions like diabetes or high blood pressure, those small co-pays can turn into big numbers. Did you know that according to 2024's national survey on prescription affordability, about 28% of Americans said they've skipped filling a prescription simply because it was too expensive? Worse, a lot of people over age 50 juggle two or more scripts a month—if they don't have insurance coverage kicking in, monthly costs can spiral past $100, even for generics.

This is where mobile prescription savings apps crashed the scene and started making a real impact. Most of these platforms work by giving users digital coupons, price comparisons, and discount cards right on their phone or computer. They're easy to use and, in most cases, totally free. Pop in a drug name, choose your pharmacy, and you get a list of real-time prices, sometimes slashing what you'd normally pay by 60-80%. The trick? Pharmacies often negotiate deals with larger buying groups or networks that these platforms tap into, bypassing the sticker price that walks-ins see.

Many folks are surprised at how painless it is to make the switch. It's not rare to see someone save $50 or more each month just by switching from paying cash to using a coupon app. That's not just pocket change. Multiply that by a family of four, and suddenly there's money left for a real dinner, a tank of gas, or back-to-school costs. Stories about patients who finally can afford their asthma inhaler or heart medication once they find an alternative to the "retail pharmacy" price are all over the internet. It’s a revolution happening quietly, one receipt at a time.

Yet, not all discount apps are built alike. Some specialize in certain conditions, others have huge pharmacy coverage, and a few even offer home delivery or telehealth consultations. The truth is, with so many choices, it can feel overwhelming. Want to see a shortlist of tested alternatives? Check out apps like GoodRx—a resource that lays out options, what they cost, and how to get started.

One thing to watch: even if you have insurance, sometimes the app’s price beats your co-pay. Don’t take the sticker on the bottle as final—run the numbers first. It’s not just for people without insurance; plenty of insured families save on prescriptions no matter what coverage they have.

Something less talked about: the impact on stress and health. People who skip out on medication often end up with bigger, costlier problems later. These apps are more than money-savers; they're health-savers. And with prescription price trends not showing signs of dropping soon, being proactive now is a strategy that pays off.

User Stories: Real Savings, Real Impact

Take Jessica, who takes medication for anxiety and migraines. She used to pay just over $100 every month, splitting pills to try to stretch her prescriptions. After a friend tipped her off to a savings app, she plugged her meds in and found discounts that dropped her bill to just $43 a month. Jessica admits, "I thought only people without insurance used these things, but my insurance co-pay was higher than the app’s coupon." The $684 she saved last year—she says that paid for a new laptop so she could take online classes. You’ll hear hundreds of stories like hers in social media groups for health and finance.

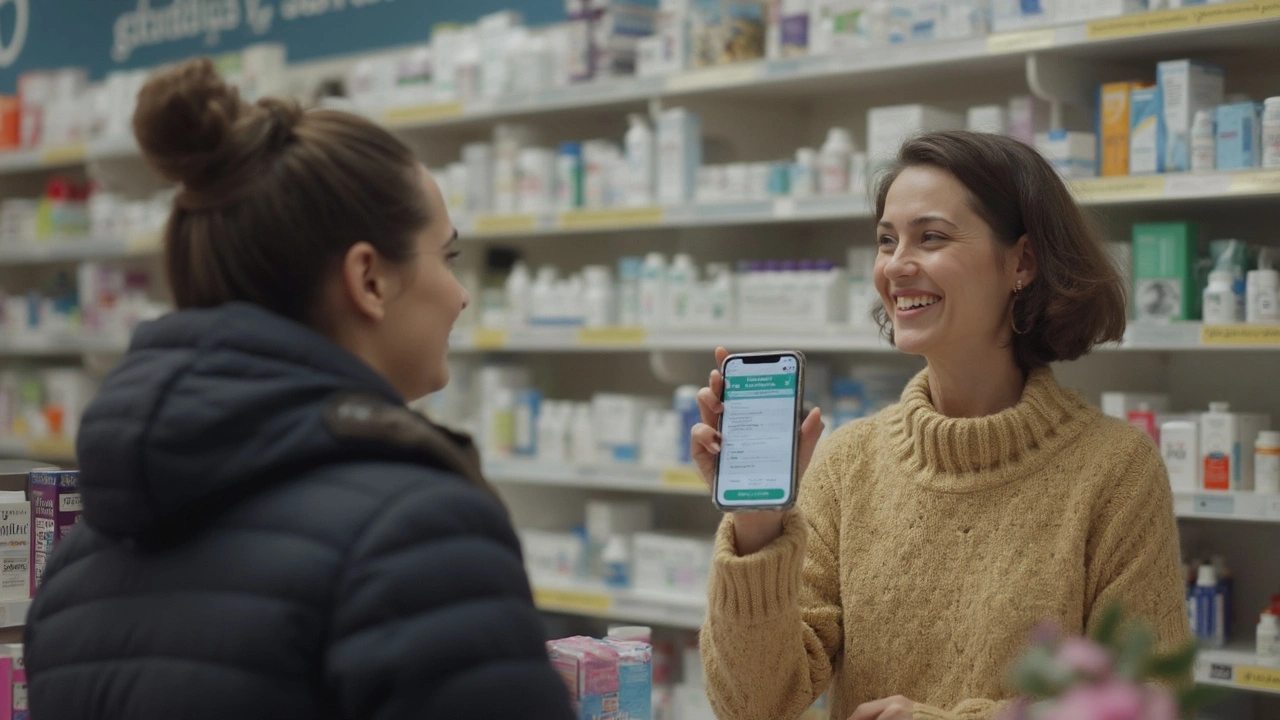

Or consider Alex, a father with a son on asthma meds. Their insurer changed their plan in January, jacking Alex’s monthly cost from $30 to almost $95. He was ready to argue with the pharmacy until a quick app search flashed up a $40 price tag. "I literally showed my phone at the counter, the tech scanned it, and the price dropped in seconds. No forms, nothing. If I’d known this months ago, I’d have saved over $600 easy." The moment he walked out, he texted the coupon to a friend whose daughter takes insulin, too. That’s the ripple effect in action.

Even in retirement communities, people are swapping savings tips. One lively Facebook group shares screenshots of their monthly receipts, comparing deals and pharmacy locations. Mary, who manages four different medications, runs all her scripts through three major savings apps before filling—one month, she stacked discounts to keep her out-of-pocket at $39 instead of $187. That’s not just luck. She uses a routine: first, sort meds in an Excel sheet, then price-check each one at three lowest-cost pharmacies within a short drive. She saves so much that she actually budgets an extra "fun" purchase every quarter—her guilty pleasure: fancy cheese at the farmer’s market.

Here’s a quick snapshot comparing monthly savings from users who switched to top-rated prescription discount apps:

| Name | Medication(s) | Old Monthly Cost | New Monthly Cost | Monthly Savings |

|---|---|---|---|---|

| Jessica | Migraine, Anxiety | $102 | $43 | $59 |

| Alex | Asthma Inhaler | $95 | $40 | $55 |

| Mary | Multiple (4 scripts) | $187 | $39 | $148 |

| Sam | Diabetes | $200 | $83 | $117 |

| Tony | Hypertension | $45 | $16 | $29 |

Notice something? These numbers aren't wild outliers. If your medication costs are even half that much, it’s real money in your pocket. More than the price, it’s the relief—knowing your next refill won’t break the bank, or that you no longer have to choose between a vital med and groceries.

If you prefer to keep things extra organized, set calendar reminders every month to check your meds online before hitting the pharmacy. Pharmacies can change prices without warning—even week to week. Some users have said one Walgreens across town was $20 cheaper than the one seven minutes away. It pays (literally) to comparison shop.

Choosing and Using the Right App: Pro Tips for Maximum Savings

It might sound too good to be true: download an app, type in your prescription, and watch your price drop. But there are ways to play it smart and squeeze even more out of these savings platforms.

- Compare more than one app – Not every app has the same discounts. Sometimes GoodRx leads, but other times single-pharmacy coupons or smaller apps (like WellRx or SingleCare) beat the big guys by a few bucks. Some users recommend screenshotting prices from three competitors and showing them to the pharmacist, just in case.

- Ask for the price before you pay – This one is key. Don’t hand over your insurance card first at the counter. Ask the tech to run your prescription as a "cash" sale with the app’s coupon and then see how it stacks up.

- Check the fine print – A few contracts ban stacking insurance and coupon discounts, so pick the bigger discount. Sometimes, mail-order or warehouse (Costco, Sam’s) pharmacies offer even cheaper rates with the app’s coupon, so expand your circle beyond CVS and Walgreens.

- Pay attention to refills and pill counts – Buying a 90-day supply can multiply your savings (in fact, many platforms highlight these options). If your doctor is flexible, ask if you can get a longer prescription to rack up three months of discounts in one shot.

- Keep up with updates – The best deals shift fast. App users recommend signing up for alerts, so if your drug price drops (or spikes elsewhere), you’ll know without having to price-check every pharmacy every time.

Another tip: check with your pharmacy loyalty program. Some chains, like Kroger or Rite Aid, occasionally have their own discount programs that sync up with some coupon apps—or even stack with manufacturer rebates for extra savings. All it takes is an extra question at the counter to see if they can do better.

And don’t forget about privacy. Many apps only ask for your zip code and the drug name—they don’t need your insurance, social security, or medical details. If privacy makes you nervous, look up each platform’s policy before signing up. There are even anonymous options if you want to keep things extra secure.

Feeling overwhelmed? Think of this as just one more tool in your cost-of-living toolkit. The savings from one prescription can snowball across your household. Realistically, anyone can use these apps: caregivers, parents with sick kids, retirees, or those just trying to make their paycheck last until the fifteenth. As the healthcare market gets more complicated, platforms like these put some of the power back in your hands—and your wallet gets to feel it first.

Try it out on your next refill. Screenshot your old price, run it through two or three savings apps, and see what happens at the counter. Even if you trim just $10 a month, that's $120 a year for less than five minutes of effort, and that’s a win no matter how you slice it.

Earlene Kalman

These discount apps sound like a miracle but they’re just a band‑aid. You still end up paying out of pocket and the savings are rarely as big as they claim. If you really want to cut costs, ask your doctor about generic alternatives.

Brian Skehan

What the big pharma won’t tell you is that they plant these coupon apps to keep us glued to their pricing algorithms. Every time you scan a barcode they collect data that feeds into the next price hike. It’s a subtle lock‑in that makes you think you’re saving while they tighten the squeeze. Use the apps, but stay aware of the surveillance loop.

Andrew J. Zak

It’s good to see people sharing tips on how to stretch their prescriptions A calm approach and checking multiple sources can make a real difference Keep the conversation respectful and focus on the practical steps

Dominique Watson

From a national perspective, the rising cost of medication undermines our healthcare sovereignty. It is imperative that citizens adopt home‑grown solutions such as domestic discount platforms. These tools empower individuals while reducing reliance on foreign pharmaceutical conglomerates. Moreover, they foster competition that can stimulate local market reforms. By leveraging these apps, we assert control over personal health expenditures. Such prudent behavior reflects patriotic responsibility. Let us champion these resources as part of a broader strategy to protect our nation’s well‑being.

Mia Michaelsen

Honestly, most people underestimate how much they can save by simply cross‑checking prices. The data shows that a single scan often reveals a discount of 30‑70 %. It isn’t rocket science; it’s just basic price comparison. If you haven’t tried it, you’re leaving money on the table. Trust the numbers, not the hype.

Kat Mudd

I’ve been using these discount apps for months now and I can say they’re not the miracle cure they’re sold as. The reality is that each app offers a different price list that changes daily and you have to invest time to compare them. If you skip that step you might end up paying more than the pharmacy’s advertised price. Most users think the coupon automatically beats any insurance co‑pay but that’s not always the case. You need to check the fine print and understand whether the discount applies to the brand or generic version. The apps also collect a lot of data about what you buy and where you shop which can be used to manipulate prices later. I’ve seen cases where a drug that was $20 yesterday jumps to $35 the next week without any clear reason. That’s why I recommend keeping a spreadsheet of your medication names prices and dates to spot trends. When you have that record you can negotiate with the pharmacy or ask a pharmacist for a better deal. Sometimes you can combine a manufacturer rebate with the app coupon for an even deeper discount. Don’t be fooled by flashy graphics in the app store that promise instant savings with a single tap. The truth is you still have to fill out the prescription, show the coupon and wait for the tech to scan it. If the pharmacist refuses to honor the discount you should politely ask for a manager. In most cases they will comply because they prefer to keep the sale rather than lose a customer. Overall, the apps are a useful tool but only if you treat them as part of a broader cost‑cutting strategy rather than a standalone fix.

Pradeep kumar

Integrating pharmacoeconomic analytics with real‑time discount algorithms can optimize therapeutic adherence while minimizing out‑of‑pocket expenditures. Leveraging these platforms as a decision‑support interface aligns patient-centric care pathways with value‑based pricing models. By stratifying medication cohorts and applying cost‑effectiveness thresholds, individuals can systematically identify optimal formulary options. The iterative feedback loop between prescription fulfillment and discount data fosters a dynamic equilibrium that sustains budgetary compliance. Embrace this synergy to enhance both clinical outcomes and financial sustainability.

James Waltrip

One must, with a discerning eye, recognize that the veneer of convenience offered by these apps is merely a façade for an entrenched oligarchy of pharmaceutical profiteers. The orchestrated revelation of “savings” is a calculated diversion designed to placate the masses while the true profit margins flourish unseen. It is intellectually dishonorable to accept such token discounts without interrogating the underlying power structures. Our collective moral compass demands a rigorous examination of the clandestine agreements between coupon distributors and drug manufacturers. Only through such scrutiny can we hope to reclaim agency over our health expenditures. The discourse, though often couched in casual vernacular, must retain a degree of scholarly rigour. In this context, the casual adopter is unwittingly complicit in sustaining the status quo. Let us therefore elevate the conversation beyond superficial price checks to a profound critique of systemic exploitation.

Chinwendu Managwu

Sure, those apps work fine for anyone not living under a real healthcare system 😏

Kevin Napier

Great rundown on the practical steps; keeping a spreadsheet is a smart habit that many overlook. It’s encouraging to see a detailed plan that balances caution with usability. By staying organized you’ll keep those savings steady while avoiding the data‑collection pitfalls.